Buybacks: A Turn toward Prudence, for Now

According to preliminary numbers from Standard & Poor’s, buybacks among S&P 500 components rose rose 15% in the third quarter, after a 55% decline in the second, leaving them 42% below a year earlier. Measured as a percent of GDP, buybacks are now in the same neighborhood they were last seen in in 2010—though that’s still well above where they were any time between 1998 and 2004.

Measured as a percentage of operating earnings, as in the second graph, buybacks fell to their lowest levels since 2010, 32%. Despite the increase in dollar volume, buybacks declined as a percentage of earnings because earnings were up 42% in the quarter. In the 40 quarters between 2010 and 2019, buybacks fell below 40% of earnings in just two of them; the average over that period was 53%.

And our third measure, buybacks relative to dividends, saw an uptick in the quarter, but remain at their lowest level since 2009, 88%. The second and third quarters were the only two since 2010 where traditional dividends exceeded buybacks; that was true of only half the quarters between 1998 and 2009. Between 2010 and 2020Q3, S&P firms bought back $5.7 trillion in stock and paid $3.9 trillion in dividends, a combined total of $9.6 trillion. Over the same period, earnings totaled $10.6 trillion. So, they paid out 90% of earnings to shareholders. After all these years of heavy transfers to shareholders—which, it must be said, have been very friendly to stock prices—you have to wonder why corporations don’t have better things to do with their profits. It’s as if Corporate America has become an old rentier, more interested in collecting cash than investing and innovating. Maybe this pandemic-induced reduction in buybacks marks a change of heart, but we suspect things will go back to the old ways in a few quarters.

Manufacturing, Women & Labor Pain

It was encouraging to see solid gains in manufacturing & construction in the most recent payroll numbers, occupations listed as more stable, and therefore safer. Back in spring the idea was to get such work rolling again, while skipping the stop at a bar on the way home. We’re hitting the reset button on that.

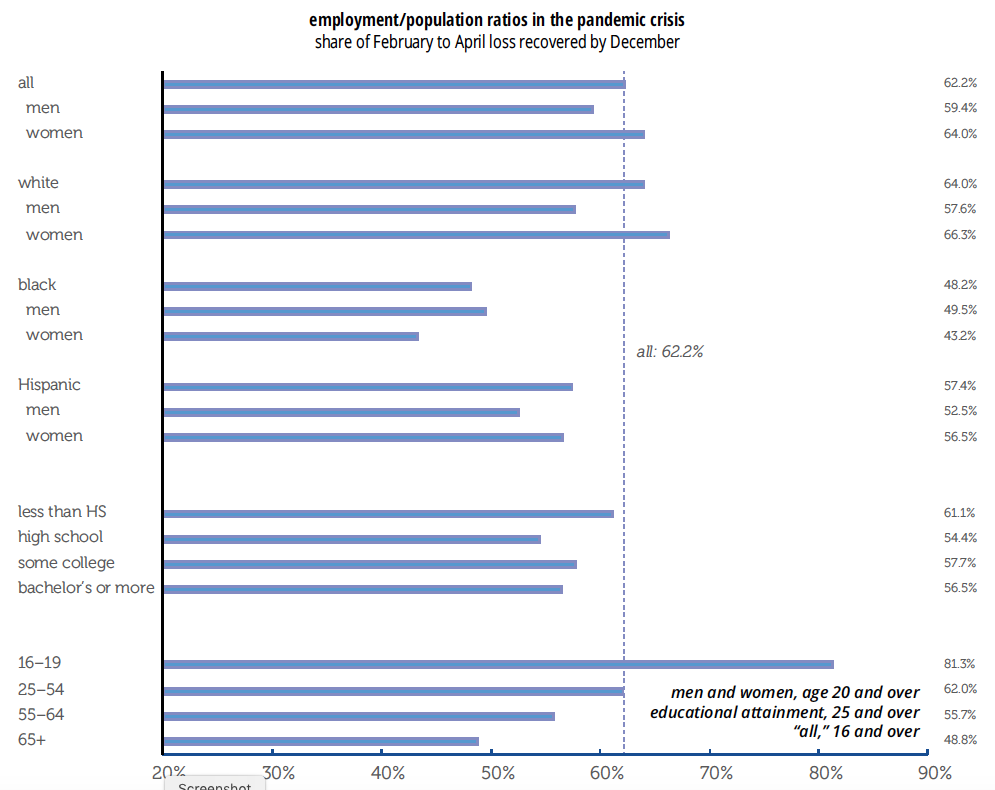

That may help get the pandemic under control, but it is going to hurt minority workers, as shown in Friday’s jobs report. The Household survey is jumpy, but the number of employed men rose, while the number of employed women fell. Within that both White and Black men gained jobs, as did White women, but Black women lost jobs, as did both sets of Latinx workers, and Asians, not broken out by sex. Gains were large enough to lift employment-population ratios for White women and Black men, while losses were enough to cause declines for Black women, Asians, and for Latinx men and women.

In 2019 women held 29% of manufacturing jobs and, within that, 39% of medical manufacturing and animal processing, 46% of sporting goods & toy manufacturing, and a little over half of textile manufacturing. Asian workers had a 7% share, but 29% of computer equipment; Blacks, 10%, and close to 20% of auto and pulp manufacturing; and Latinx, 17%, including 40% of fruit and vegetable preservation. Both Black and Latinx workers have close to 20% share in tire manufacturing, and 22% and 35% shares in animal processing plants.

Manufacturing employment is still down 4% over the year, less than overall employment’s -6%. We sometimes include a graph of the three-month average of manufacturing withholding in a classic Midwestern state. Here’s what that looks like these days: