The Biden administration’s industrial policy, specifically the CHIPS and Science Act, appears to be having a serious real-world effect. Construction in the computers and electronics sector is setting records, and by a wide margin.

The CHIPS (“Creating Helpful Incentives to Produce Semiconductors”—why do they find acronyms so irresistible?) Act was designed to bring semiconductor manufacturing back to the US. It was inspired by supply chain lessons from the pandemic—maybe having to source crucial industrial supplies from halfway around the world isn’t as brilliant an idea as it seemed at first—and to wean American industry from Chinese component makers as tensions between the two countries mount. According to a McKinsey summary, the law “directs” about $280 billion in new investments and R&D in the sector over the next ten years, via a mix of direct spending and tax breaks. Some $24 billion of that is devoted to tax credits designed to stimulate investment in semiconductor manufacturing.

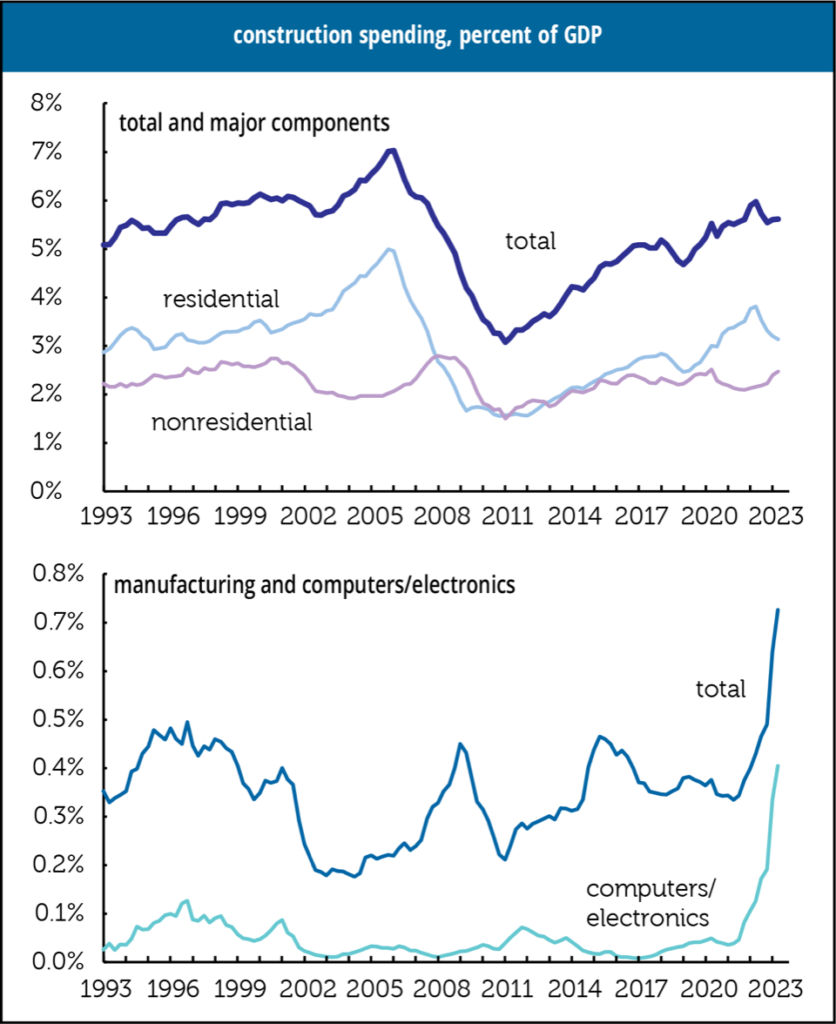

If you look at the Census Bureau’s construction spending numbers, the bipartisan Act is already stimulating such investment. Graphed below are quarterly averages of monthly spending numbers (which are expressed as a seasonally adjusted annual rate) as a percent of GDP. The top graph shows the total and major aggregates, which fall well short of the “eye-popping” modifier. Residential construction has risen, first with the recovery from the 2006–2012 housing bust, and then accelerating with the 2020–2022 boom—though the 2022Q2 peak, 3.8% of GDP, was no match for 2005Q4’s 5.0%. Nonresidential has been pretty flat for almost a decade, only recently returning to its pre-pandemic levels.

But the second graph tells a very different story: a surge in manufacturing, largely accounted for by computers and electronics. The slope of the lines does qualify for the “eye-popping” modifier, as do the numbers behind the picture. Between 2021Q4 and 2023Q2, construction spending in manufacturing is up 114%, with 86% of the dollar increase coming from the computers and electronics subsector, where spending is up 441%. That surge took construction spending in computers and electronics from 0.1% of GDP to 0.4%. That may not sound like much, but it never got above 0.1% until 2022Q3. No other manufacturing subsector reported by Census shows an increase unless you take it out to two decimal places.

What will come of this spending won’t be known for some time. But something is happening now.

More Info...

Subscribe >

More Info...

Subscribe >

More Info...

Subscribe >

More Info...

Subscribe >

Tech Construction Boom

The Biden administration’s industrial policy, specifically the CHIPS and Science Act, appears to be having a serious real-world effect. Construction in the computers and electronics sector is setting records, and by a wide margin.

The CHIPS (“Creating Helpful Incentives to Produce Semiconductors”—why do they find acronyms so irresistible?) Act was designed to bring semiconductor manufacturing back to the US. It was inspired by supply chain lessons from the pandemic—maybe having to source crucial industrial supplies from halfway around the world isn’t as brilliant an idea as it seemed at first—and to wean American industry from Chinese component makers as tensions between the two countries mount. According to a McKinsey summary, the law “directs” about $280 billion in new investments and R&D in the sector over the next ten years, via a mix of direct spending and tax breaks. Some $24 billion of that is devoted to tax credits designed to stimulate investment in semiconductor manufacturing.

If you look at the Census Bureau’s construction spending numbers, the bipartisan Act is already stimulating such investment. Graphed below are quarterly averages of monthly spending numbers (which are expressed as a seasonally adjusted annual rate) as a percent of GDP. The top graph shows the total and major aggregates, which fall well short of the “eye-popping” modifier. Residential construction has risen, first with the recovery from the 2006–2012 housing bust, and then accelerating with the 2020–2022 boom—though the 2022Q2 peak, 3.8% of GDP, was no match for 2005Q4’s 5.0%. Nonresidential has been pretty flat for almost a decade, only recently returning to its pre-pandemic levels.

But the second graph tells a very different story: a surge in manufacturing, largely accounted for by computers and electronics. The slope of the lines does qualify for the “eye-popping” modifier, as do the numbers behind the picture. Between 2021Q4 and 2023Q2, construction spending in manufacturing is up 114%, with 86% of the dollar increase coming from the computers and electronics subsector, where spending is up 441%. That surge took construction spending in computers and electronics from 0.1% of GDP to 0.4%. That may not sound like much, but it never got above 0.1% until 2022Q3. No other manufacturing subsector reported by Census shows an increase unless you take it out to two decimal places.

What will come of this spending won’t be known for some time. But something is happening now.