We are happy to report that Hale Stewart will be contributing to our blog going forward. Here’s a longer look from him, with an assist from the St. Louis Fed, at pricing trends.

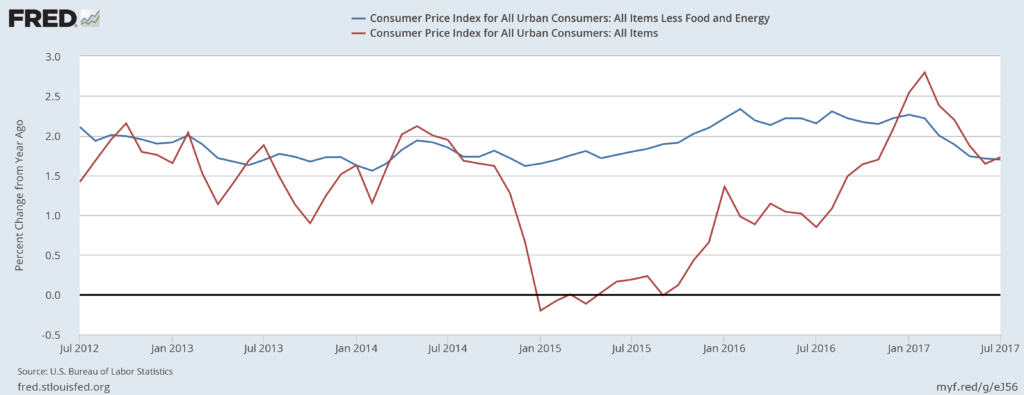

Friday’s inflation report was, yet again, underwhelming, further confirming that upward price pressures are contained. Core and overall CPI are 1.7% Y/Y:

Both measures are below the Federal Reserve’s 2% inflation target. Core (in blue) was slightly above 2% for most of 2016 while total CPI (in red) was rising. But its increase did not influence overall CPI, indicating that commodity pressures are weak. Although they are part of the misery index, neither food nor energy prices should concern us in terms of sticky inflation:

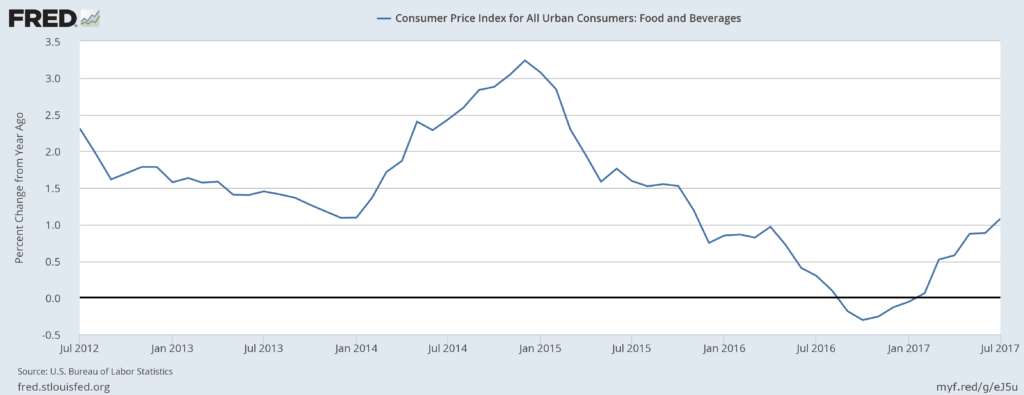

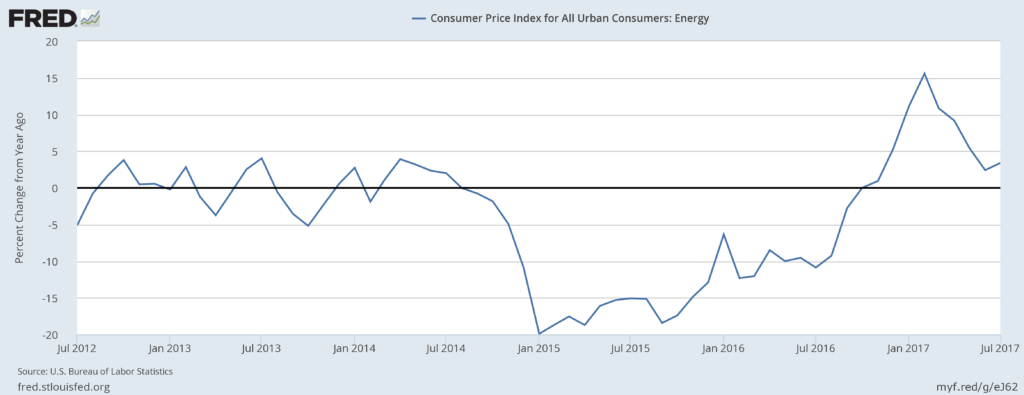

The top chart shows the year Y/Y percentage change in food and beverage prices, which were declining from the beginning of 2015 to 3Q2016. They are now increasing, but are only slightly above 1%. The bottom chart shows energy prices which were negative for approximately two years, turning positive at the beginning of 2017. Yes, they did spike to about 15%, but that’s as much a function of statistics as the marketplace activity. Now they are quickly declining. Just as importantly, food and beverage prices are only 13.63% of CPI while energy prices are 7.35%, meaning both would have to increase at sharply faster rates for an extended period time for us to be concerned.

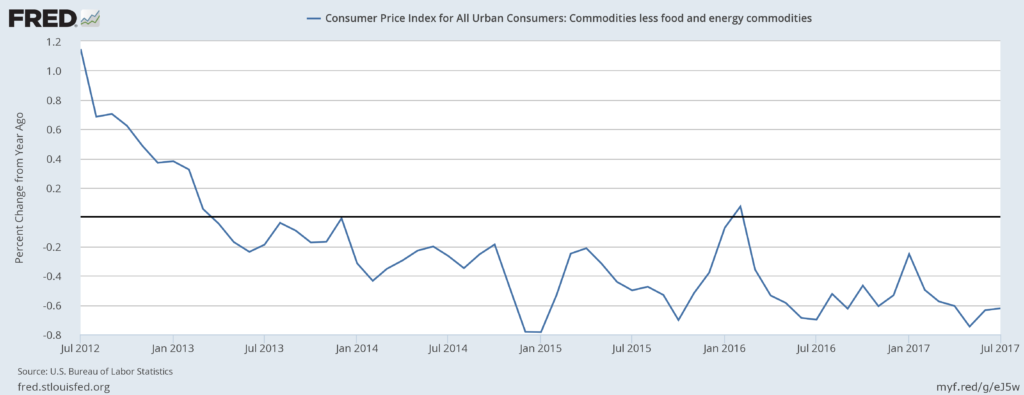

Energy and food prices are the only commodity prices adding to CPI:

All commodities less these two items have subtracted from CPI for over four years. This sub-index of overall CPI accounts for 18.95% of CPI. Its negative contributions counterbalance any upward pressure from food and energy prices.

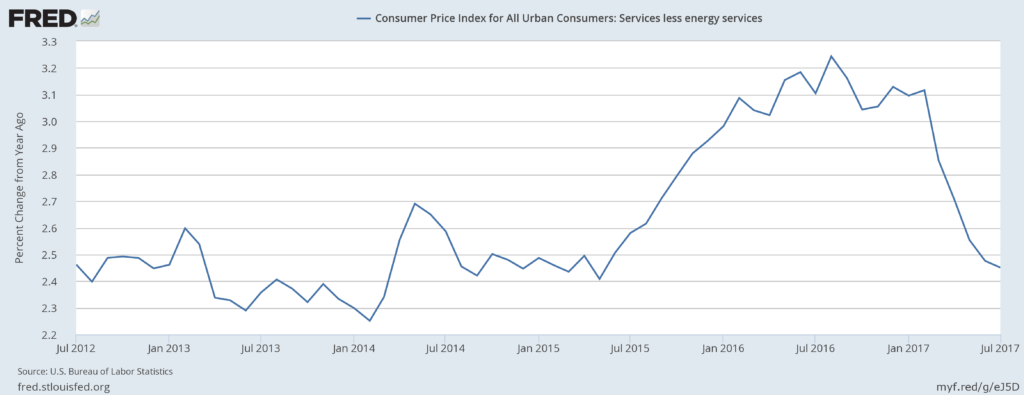

Finally, we have the sub-index for services less energy:

This was between 3%-3.2% for most of 2016, but has since decreased sharply. The underlying reasons for this spike have dissipated.

Readers sometimes suggest we adjust spending measures, like retail sales, for certain segments’ own personal deflation in order to show that spending is actually quite strong. That gets a “Huh?” from us. If spending were strong, prices would be floating up. The point is that they are not.

More Info...

Subscribe >

More Info...

Subscribe >

More Info...

Subscribe >

More Info...

Subscribe >

Inflation, that dog just won’t bark

We are happy to report that Hale Stewart will be contributing to our blog going forward. Here’s a longer look from him, with an assist from the St. Louis Fed, at pricing trends.

Friday’s inflation report was, yet again, underwhelming, further confirming that upward price pressures are contained. Core and overall CPI are 1.7% Y/Y:

Both measures are below the Federal Reserve’s 2% inflation target. Core (in blue) was slightly above 2% for most of 2016 while total CPI (in red) was rising. But its increase did not influence overall CPI, indicating that commodity pressures are weak. Although they are part of the misery index, neither food nor energy prices should concern us in terms of sticky inflation:

The top chart shows the year Y/Y percentage change in food and beverage prices, which were declining from the beginning of 2015 to 3Q2016. They are now increasing, but are only slightly above 1%. The bottom chart shows energy prices which were negative for approximately two years, turning positive at the beginning of 2017. Yes, they did spike to about 15%, but that’s as much a function of statistics as the marketplace activity. Now they are quickly declining. Just as importantly, food and beverage prices are only 13.63% of CPI while energy prices are 7.35%, meaning both would have to increase at sharply faster rates for an extended period time for us to be concerned.

Energy and food prices are the only commodity prices adding to CPI:

All commodities less these two items have subtracted from CPI for over four years. This sub-index of overall CPI accounts for 18.95% of CPI. Its negative contributions counterbalance any upward pressure from food and energy prices.

Finally, we have the sub-index for services less energy:

This was between 3%-3.2% for most of 2016, but has since decreased sharply. The underlying reasons for this spike have dissipated.

Readers sometimes suggest we adjust spending measures, like retail sales, for certain segments’ own personal deflation in order to show that spending is actually quite strong. That gets a “Huh?” from us. If spending were strong, prices would be floating up. The point is that they are not.